| Back to Tax School Homepage | ||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||

|

Federal Tax Law |

||||||||||||||||||||||||||||||||

|

Table of Contents |

||||||||||||||||||||||||||||||||

|

Constitutionality of Taxation Some Tax History Budget Proposal Annual Inflation Adjustments Information on Your Tax Return Increase in the Standard Deduction Change in Filing Requirements for Each Filing Status Temporary Reduction of Personal Exemption to Zero Filing Requirements Recordkeeping Requirements How Long to Keep Records? Filing Status Head of Household The Correct Form From 1040EZ Form 1040A Taxpayer Identification Numbers Adoption Taxpayer Identification Numbers Practitioner PIN Change of Name Identity Theft Married Filing Separate Relief of Liability Married Filing Jontly Married But Considered Unmarried Common Law Marriage Same Sex Marriage Itemized Deductions Schedule A Medical Expenses State and Local Tax Deduction and Limit Home Mortgage Interest Deduction Changes Charitable Contribution Changes AGI Limit for Cash Contributions No Deduction for Athletic Tickets Repeal of Exception to Contemporaneous Written acknowledgement Casualty and Theft Los Deduction Limited to Only Federally Declared Disaster Areas Suspension of Miscellaneous Itemized Deductions Subject to 20% of AGI Suspension of Overall Limitation of Itemized Deductions Itemized Deductions or the Standard Deduction Qualifying Widow (or Widower) Standard Deduction for Dependent Single Taxability of Earnings 2018 Tax Rates and Income Brackets Employee Fringe Benefits Income Tip Income Interest Income Schedule B, Part III Foreign Accounts and Trusts Requ irementsKiddie Tax State Refunds Schedule C Self-Employment Schedule C Provisions Elimination of Entertainment Expenses Definition of Income and Expenses New Section 179 Expense Limits 100% Expending (Bonus Depreciation) Luxury Auto Limits Listed Property Real Property Depreciation 20% Deduction for Pass-Through Entities Net Operating Loss (NOL) Business Vs Hobby Business Use of Home Capital Gains and Losses What is a Capital Asset? Unemployment Compensation Retirement Income Social Security Benefits IRA/401(k) Distributions Pensions Annuities Roth IRA Recharacterization Rules Adjustments to Income Moving Expenses Suspended Direct Deposit Underpayment Penalty Failure to File Frivolous Tax Return Automatic Extension of Time to File Individual Retirement Accounts Lump Sum Distributions Statute of Limitations Amending Your Tax Return Decedents Credit for Child and Expenses Credit for the Elderly or the Disabled Alimony Estimated Tax Payments Additional Medicare Tax Net Investment Income Tax Taxable and Nontaxable Income Schedule B Section 529 Plan Changes Achieving a Better Life Experience (ABLE) Account Discharge of Certain Student Loan Indebtedness Earned Income Credit Credits Enhanced Child Tax Credit Credit Eligibility SSN Requirement New Nonrefundable Child Tax Credit Education Child and Dependent Care Credit Tax Withholding and Estimated Tax Payments Balance Due and Refund Options Affordable Care Act (ACA) Provisions Share Responsibility Payment Individual Mandate Penalty Eliminated Alternative Minimu m Tax (AMT)Tax Return Due Date References Review Questions Final Exam |

||||||||||||||||||||||||||||||||

| Constitutionality of Taxation | ||||||||||||||||||||||||||||||||

|

When new tax laws pass, you as

a taxpayer always have the opportunity to challenge these laws. Just like

other laws, tax laws can be challenged.

Can you believe there was a time when there was no income tax? We were at one time with no tax laws. Our tax collectors were merely an extension of the English tax collectors. As a new nation, we had to come up with new laws and many of these laws copied over from the old world. Then, we had to make sure that our new laws and tax laws were in accord with other documents such as the Constitution. For a long time, there was no provision in the Constitution to tax individuals and the taxing of individuals was considered unconstitutional. The taxing process graduated slowly to what it is now. Although at one point there was a question of the constitutionality of taxation, it was just a matter of minor adjustments. Taxes are a necessity. How else can we survive and prosper as a nation? |

||||||||||||||||||||||||||||||||

|

Can you believe there are individuals who are still trying to

fight the constitutionality of taxation?

This fight on whether taxing individual being unconstitutional has kept going. There are still organizations that are trying to keep this concept of taxes being unconstitutional alive. The IRS time and again excuses these arguments as frivolous tax arguments and as mere misinterpretations of laws and of the Constitution. This has been going on since the start. For example, in 1895, the U.S. Supreme Court decided that the income tax was unconstitutional because it was not apportioned among the states in conformity with the Constitution. More recently in 2004, the U.S. was forced to eliminate a corporate tax provision that had been ruled illegal by the World Trade Organization. Two tax bills signed in 2005 and 2006 extended through 2010 the favorable rates on capital gains and dividends that had been enacted in 2003, raised the exemption levels for the Alternative Minimum Tax, and enacted new tax incentives designed to persuade individuals to save more for retirement. |

||||||||||||||||||||||||||||||||

| Some Tax History | ||||||||||||||||||||||||||||||||

| Sometimes is helps to know some history about the items we deal with. If you know the history of taxation, you have a conversation piece for your customers to make things more interesting. Makes everything so much easier to understand and to explain when you know the history behind the entire thing. Many changes have occurred since Congress enacted the first income tax law. In 1862, Congress enacted the nation's first income tax law in order to support the Civil War effort. It was in 1862 that the office of Commissioner of the Internal Revenue was established. It was then that this individual was given the power to enforce the tax laws. There has not been too much change to this power to now. The Act of 1862 established the office of the Commissioner of Internal Revenue. The Commissioner was given the power to assess taxes, to enforce the tax laws through seizure of property and income and prosecution and to levy and collect taxes. | ||||||||||||||||||||||||||||||||

|

Many individuals have tried to influence these new tax laws. Many times the tax laws were changed and amendments issued to make the tax laws a permanent component of our daily life. Taxes are here to stay and will be raised as the need arises for more money. The fact remains that the powers and authority of the office of Commissioner of Internal Revenue remain very much the same today. However, there is a difference now and it has to do with the media. Today the taxpayer seems to have more power due to social media and the knowledge and advice inseminated by others through the internet. Those books with titles such as "How To Beat the IRS" are real and they offer much advice on how to win your case against the IRS. Some people call these dirty attorney tricks. Regardless of what they are called they still provide guidance and information on Internal Revenue loopholes. They still provide information on IRS operations and loopholes in the tax law regardless if you are going to use the loopholes to be unethical. |

||||||||||||||||||||||||||||||||

|

By 1913, the 16th Amendment to the Constitution made the income tax permanent as we have it today. This amendment gave Congress legal authority to tax income of both individuals and corporations. Amendments like the one in 1913 are brought about through the needs for additional funds of government. Also, many tax changes are incepted due to economy changes such as more employment available to taxpayers or vice versa. If there is high unemployment, then tax laws will take that into consideration too. This is done so and mostly seen by the tax credits or special tax deductions offered though the tax system. |

||||||||||||||||||||||||||||||||

| President Reagan made a huge contribution to our current tax laws. For example on October 22, 1986, President Reagan signed into law the Tax Reform Act of 1986. The act called for an decrease in individual taxation over a five-year period. Over the years, the tax laws got so complicated that there was a need to simplify the tax code. The tax code and the paperwork to file a tax return was a difficult bureaucratic effort. Additionally, President Reagan wanted to up the economy with his tax law reform. We are living this tax reform presently. With this October 22, 1986 law that President Reagan signed into law the Tax Reform Act of 1986, the top rate on individual income was lowered from 50% to 28%. | ||||||||||||||||||||||||||||||||

|

Later on and in an effort to reduce the federal budget deficit, the Revenue Reconciliation Act of 1990 was signed into law on November 5, 1990. The emphasis of the 1990 act was increased taxes on the wealthy. It came to everyone's realization that the wealthy were paying less than the fair share. With this new act came higher taxes and a limitation on itemized deductions. Almost every presidential candidate promises not to raise taxes. President Bush promised not to raise taxes to get elected and then signed the Revenue Reconciliation Act of 1990 in law which did the contrary. It raised taxes and lowered deductions. This was the act that started our "pay as you go system". In this system taxpayers pay their tax in installments as they earn the money. This is usually done weekly or biweekly every time the taxpayer receives a check from their employer. Taxpayers who don't have an employer usually are required to make estimated tax payments throughout the tax year. Other countries have similar tax policies. |

||||||||||||||||||||||||||||||||

| Again, in 1993 another act was signed to lessen the tax deficit. On August 10, 1993, President Clinton signed the Revenue Reconciliation Act of 1993 into law. What was different about the 1993 act to the 1986 was that the Revenue Reconciliation Act of 1993 affects almost every taxpayer, not only the rich. This new tax act decreased the tax planning benefits and tax planning strategies previously enjoyed by many. | ||||||||||||||||||||||||||||||||

| Then again in 1997, President Clinton signed a tax revenue act which cut taxes by $152 billion including a cut in capital gain tax for individuals a $500 per child tax credit along with tax incentive for education. This per child tax credit has now increased to $1,000 per child. The child tax credit started at $400 per child and increased to $500 per child in 1999. It was with this act that Roth IRAs were established. This act also exempted the capital gain taxation of the sale of personal residences of up to $500,000 for married couples and up to $250,000 for single taxpayers. There is also a $600,000 estate tax exemption and family farms and small businesses can qualify for exemption of $1.3 million. It was also at this time that the annual gift tax was corrected for inflation. | ||||||||||||||||||||||||||||||||

|

We have come a long way from 200 years ago. From 1791 to 1802, the United States government was supported by internal taxes on distilled spirits, carriages, refined sugar, tobacco and snuff, property sold at auction, corporate bonds, and slaves. Now, the government gets their review from more modern items in addition to the items from 100-200 years ago. This includes more modern items such as commerce transacted over the internet and plastic surgery tax. This all started in 1791. Before that really. Way before that in some form or other. It is just that things become formal at one point or other. In 1862, in order to support the Civil War effort, Congress formally enacted the nation's first income tax law and it was a forerunner of our modern income tax. The nation's first sales taxes were on gold, silverware, jewelry and watches due to the high cost of the War of 1812. This war resulted in struggles. Individuals did not only have to worry about certain war uncertainties, but by this time they also had to worry about complying with the government and pay tax. During the Civil War, a person earning from $600 to $10,000 per year paid tax at the rate of 3%. |

||||||||||||||||||||||||||||||||

|

Many things have transpired in the process of a more fair tax. Beginning in 1868, Congress focused its taxation efforts on tobacco and distilled spirits and eliminated the income tax in 1872. Tobacco laws have changed and it started from tax making money from producing it to trying to complete eradicate the habit. The government has recently become concerned with public health and has passed certain taxes on tobacco products to discourage their consumption. Now the government is trying to discourage tobacco product consumption by charging high taxes on the products. Others tax changes have transpired in the process of candidates to office wanting to get elected or re-elected to office. |

||||||||||||||||||||||||||||||||

| Budget proposal | ||||||||||||||||||||||||||||||||

|

Everyone needs a budget, even the United States Treasury. On or before the first Monday in February of each year the President is required by law to submit to Congress a budget proposal for the fiscal year that begins the following October. The United States budget process was initiated in 1921 and it was not a formal process. It was until 1974 that Congress was forced to adopt a more formal process. The Congressional Budget and Impoundment Control Act of 1974 was enacted because President Richard Nixon refused to spend funds as Congress had allocated them and passing a more formal budget process would force President Nixon to spend funds as Congress had indicated. |

||||||||||||||||||||||||||||||||

|

On December 22, 2017, the Tax Cuts and Jobs Act was passed by Congress. This new tax act provided reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018”. This legislation, which the President signed into law on Dec. 22, 2017, is the most sweeping tax reform measure in over 30 years. The new legislation makes fundamental changes to the Internal Revenue Code that will completely change the way individuals and businesses calculate their federal income tax liability, so as to create numerous planning opportunities. The changes affecting individuals include new tax rates and brackets, an increased standard deduction, elimination of personal exemptions, new limits on itemized deductions (state taxes, mortgage interest), and the repeal of the individual mandate under the Affordable Care Act. The changes affecting businesses include a reduction in the corporate tax rate, increased expensing and bonus depreciation, limits on the deduction for business interest, and a new 20% deduction for pass-through business income. The foreign provisions include an exemption from U.S. tax for certain foreign income and the deemed repatriation of off-shore income. This new tax reform is the new Tax Cuts and Jobs Act (TCJA). This new tax reform was passed to take effect on both individuals and businesses. This new legislature dictates how businesses compute business interest and what business interest limitations exist under the new legislation recently passed on December 22, 2017. This new tax law will also affect the withholding on the transfer of non-publicly traded partnership interests and tax withholding me need adjustment for certain key groups. Furthermore, the new legislation affects the computing of the "transition tax" on the untaxed foreign earnings of foreign subsidiaries of U.S. companies. S corporations are also subject to the extended three year holding period for applicable partnership interests. With the new tax law changes, will come different withholding demands. The interest on home equity loans will still be deductible under the new tax law. Other items will be affected, such as the procedures for changing the accounting period of foreign corporations owned by U.S. shareholders that are subject to the transition tax under the new Tax Cuts and Jobs Act. Certain 2018 Pension Plan limitations will not be affected by the new tax law of 2017. The new law will not affect tax year 2018 dollar limitations for retirement plans. Alaska Native Corporations and Alaska Native Settlement Trusts may be able to take advantage of certain benefits that are in place in the new tax law legislation. Certain tax advantages may exist is paying items early before enacting of certain items in the new tax code take effect. One of these items is prepaid real property taxes. Real property taxes may be deductible in 2017 if assessed and paid in 2017. |

||||||||||||||||||||||||||||||||

| Annual inflation adjustments | ||||||||||||||||||||||||||||||||

|

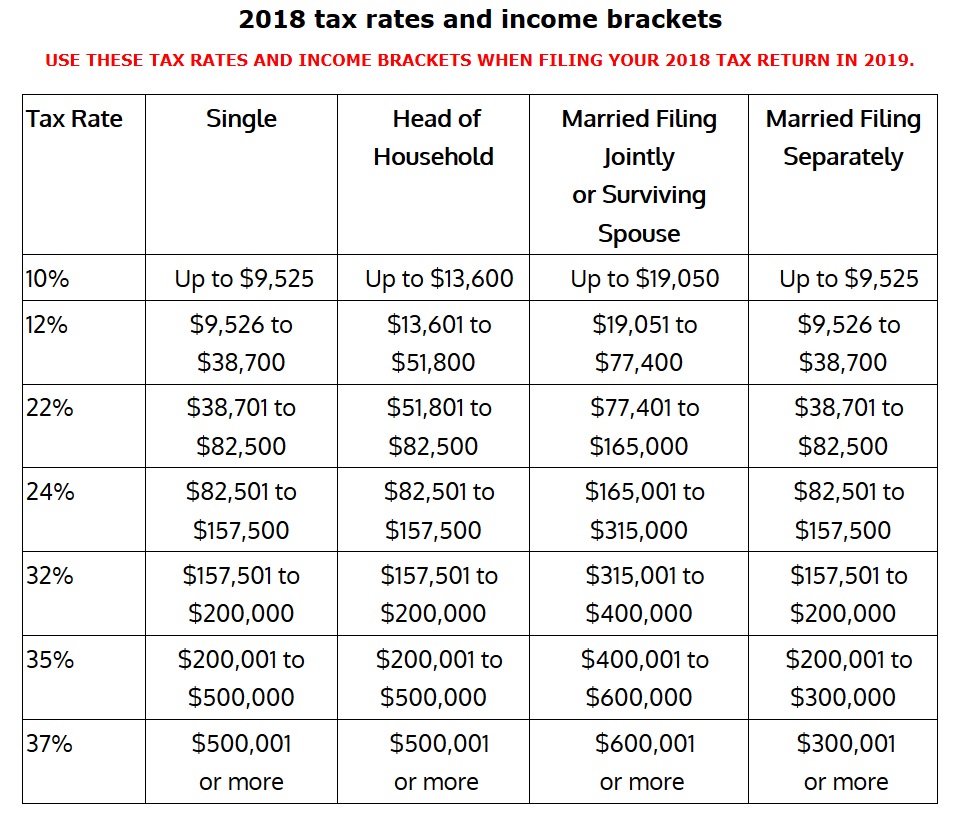

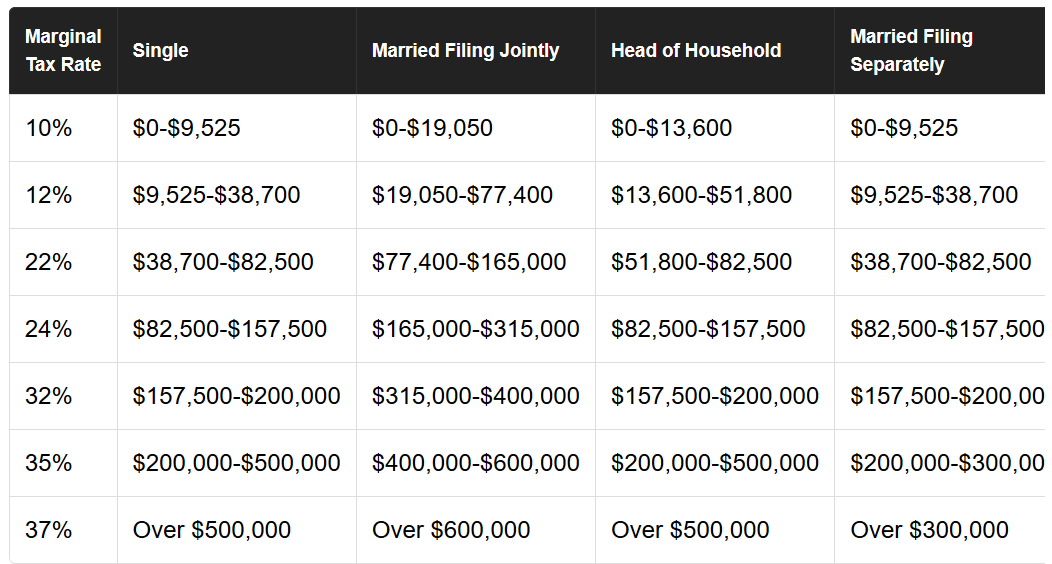

New tax law – new way to calculate inflation. We can measure the consumer price index by looking at the average price of the most common household goods and services. The results compared to previous results give us information about our economy – inflation or deflation. This tells us if the economy is good or if it is not doing so well. By inflation we mean rising prices and by deflation we mean falling prices. However, for our purpose of tax law changes, the new tax law will disregard the CPI index as a measure of inflation. The new tax bill will switch the calculation of inflation. The new tax law will now use the Chained CPI which grows slower than the traditional consumer price index. The Chained CPI use the same common household goods but if the particular goods or services get to expensive, it is assumed that consumers will select other cheaper products and thus use a cheaper alternative. The Chained CPI as a means to calculate inflation is supposed to be one of the positive items in the new tax law changes. What that means to individuals is that the income thresholds for each marginal tax bracket will rise more slowly than in previous years. Or is it? At first maybe, but this will not be so in later years. The new way will make a greater portion of each worker’s income subject to higher marginal tax rates in the long run. This could turn out to be disastrous for the middle class as it is expected to result in higher taxes. The TCJA tax reform has replaced the existing tax rates with seven new rates. These rates are 10%, 12%, 24%, 32%, 35% and the highest one at 37%. The TCJA tax reform amended section 11(3) to provide a permanent cost-of-living adjustment based on the Chained Consumer Price Index for All Urban Consumers (C-CPI-U). The Cost of living index is modified by Rev. Proc. 2018-18 and it modifies certain 2018 cost-of-living adjustments set forth to reflect statutory amendments made by an Act to provide reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018. The TCJA tax reform section 22021 amends section 63(c)(2) to provide a temporary increase in the basic standard deduction for taxable years after December 31, 2017 and before January 1, 2026. The following are the new basic standard deductions.

The older or blind individuals will continue to receive an additional amount added to their standard deduction. For those who are age 65 or older, the additional amount is $1,300 for 2018 or $1,600 if the individual is also unmarried and not a surviving spouse. Deductions considerations are based, according to the IRS, on inflation. It may be better for now on to use the standard deduction amounts since they are really high and your itemized deductions, especially with some of the new limitations or straight out elimination of certain deduction will probably not be more than the standard deduction amount. These amounts will remain similar except for adjustments for inflation for taxable years after December 31, 2018. The personal exemption which is normally adjusted for inflation every year has been changed by the TCJA to $0. Inflation works by taking a percentage of the inflation increase, but no matter how you put it, anything percent of $0 will always be $0. This is to remain from January 1, 2018 through December 31, 2026. So now we have a new way to inflation using the consumer price index. We measure the consumer price index by looking at the average price of the most common household goods and services. This new way is supposed to be a more exact manner in which we measure inflation and it will be used from now on or at least until December 31, 2026. The new way is the Chained CPI which grows slower than the traditional consumer price index. The TCJA tax reform has also replaced the existing tax rates with seven new rates. These rates are 10%, 12%, 24%, 32%, 35% and 37%. This is probably where everyone is getting the idea that this tax reform is for the rich - the lowest tax rate of 10% remained at 10% while all the others changed at least a little. The lower tax rates will compensate for the fact that we no longer can use the exemption credits for having dependents, but not for the ones at the lower 10% bracket. No more effort needs to be made in adjusting the personal exemptions for inflation as done every year since there is none. |

||||||||||||||||||||||||||||||||

| Information on your tax return | ||||||||||||||||||||||||||||||||

|

The information asked on your tax return is needed to carry out the tax laws of the United States and to figure and collect the right amount of tax. It is imperative that you supply the taxing agencies with the most correct information requested on the tax forms and worksheets. Form 1040EZ, Form 1040A and Form 1040 ask you for information about yourself, your spouse if you are married, and your dependents. |

||||||||||||||||||||||||||||||||

| In turn, the Internal Revenue Service uses the information you supply to calculate the amount of tax you should have been paying throughout the year and therefore the correct amount of tax to collect. The Internal Revenue Service also uses this information to determine if you qualify for the credits and deductions you are claiming on your tax return. | ||||||||||||||||||||||||||||||||

| Many tax preparers are failing to provide the extra information needed on tax returns such as contact phone number. What are they thinking? That it is there for decoration? Some information on tax returns is absolutely imperative and your tax return will not be processed without it. The return that is missing such important information will be returned to the taxpayer and thus the filing of your tax return will be delayed. The filing of the return may also be considered late if such information is missing because usually the Internal Revenue Service will simply send back the entire return for corrections to be made. Be careful when you fill out those forms to avoid any trouble with the Internal Revenue Service. | ||||||||||||||||||||||||||||||||

| Increase in the Standard deduction and change in filing requirements for each filing status | ||||||||||||||||||||||||||||||||

| The new Tax Cuts and Jobs Act will increase the standard deduction amount to $12,000 for individuals, to $18,000 for head of household and to $24,000 for married couples filing jointly and surviving spouses. If you are age 65 or over, blind or disabled, you can add on $1,300 to your standard deduction if you are single, or an extra $1,600 if you are married. For individual taxpayers, you will be required to file a tax return if your gross income for the taxable year is more than the standard deduction. If you are married, you would add your spouse’s income to the picture and if the income added together is more than the standard deduction for married filing jointly, you must file a tax return. | ||||||||||||||||||||||||||||||||

| Temporary reduction of personal exemption to zero | ||||||||||||||||||||||||||||||||

| The personal exemption which is normally adjusted for inflation every year has been changed by the TCJA to $0. Inflation works by taking a percentage of the inflation increase, but no matter how you put it, anything percent of $0 will always be $0. This is to remain from January 1, 2018 through December 31, 2026. | ||||||||||||||||||||||||||||||||

| Filing requirements | ||||||||||||||||||||||||||||||||

|

Everyone who makes money must file a tax return for the most part. Some will be exempt from filing if their income does not fall within certain guidelines. Filing your tax return will most probably be obligatory. However, sometimes it will be in your best interest to file even if filing is not mandatory. |

||||||||||||||||||||||||||||||||

| You must determine your filing status before you can determine whether you must file a tax return, your standard deduction and your tax. | ||||||||||||||||||||||||||||||||

| Whether you must file a federal income tax return depends on many factors such as your gross income, your filing status used, your age and whether you are a dependent. If you are required to file a tax return but you fail or willfully fail to do so you may have to pay a penalty. Not filing your return is serious business and you could be subject to criminal prosecution for choosing to not file. | ||||||||||||||||||||||||||||||||

| You must always determine your filing status before you can determine your filing requirements, standard deduction and thus your correct tax. Your filing requirements are based on your filing status. You can always file a tax return, but you are not always obligated to do so. You want to file a tax return when you are due a refund for example. For tax year 2018, you must file a tax return if you are single (under age 65) and your income was at least $12,000. You must file a tax return if you are Head of household (under age 65) and your income was at least $18,000. You must file a tax return if you are married filing jointly (one spouse was over age 65) and your income was at least $25,600. Furthermore, once you determine if you are single, married filing jointly or married filing separately, head of household, then you can look up the amount that corresponds with your filing status. Based on all these, again by looking in the correct tables or using the correct tax rates, you can determine the correct tax to pay. | ||||||||||||||||||||||||||||||||

| Besides the income level guidelines, you must also file a tax return if you have other circumstances present. For example if you owe special taxes such as the alternative minimum tax (AMT). If you owe taxes on individual retirement accounts (IRAs), you most likely will be under obligation to file a tax return. If you had social security or Medicare taxes on tip income that you did not report to your employer, then you must file to pay your share of these taxes. Other situations in which you must file a tax return is when you have write-in taxes such as uncollected social security, Medicare, or railroad retirement tax on tips your reported to your employer. Additionally, you must file a tax return if you have write-in taxes on group-term life insurance and additional tax on health savings accounts. You must also file if you have household employment taxes. However, if you only have household employment taxes and nothing else, then just need to file Schedule H by itself. You must also file if you have any type of recapture taxes. | ||||||||||||||||||||||||||||||||

| There are many circumstances where you must file a tax return even if the amounts you are dealing with are small amounts. Any special circumstances aside from plain Form W-2 wages usually obligate you to file. For instance, if you received Archer MSA, Medicare Advantage MSA, or health savings account distributions, then you must file a tax return. If you had earning from self-employment of at least $400 then you are liable for social security taxes and must file to pay your fair share. If you worked for a church or any qualified church-controlled organization and you had wages from these of at least $108.28 then for sure you will be obligated to file a tax return. More recent legislation, if advance payments of the premium tax credit were made to you or your spouse or dependents as a result of being enrolled through the Health Insurance Marketplace, you must file a tax return. If you had any of these advanced payments you will see them on Form 1095-A from such organization. | ||||||||||||||||||||||||||||||||

| Even if you do not have to file a tax return, you should file one to get a refund of any federal income tax withheld or you are eligible for the Earned Income Tax Credit. Also, just because you hardly made any money does not mean that your employer has not withheld anything from your check. Depending on how many deductions you claimed on your Form W-4, you may have had federal tax withheld from your check. Almost everyone pays social security and Medicare taxes and these are not the kind of taxes you can get refunded. However, if you had federal withholding or any state tax withheld, you can file your federal or state tax returns to get these refunded to you if you did not make enough money to even file a tax return. Why would your employer if withhold any money in the first place? You ask. Well, when you first start your job, your employer usually does always get your Form W-4 from you right away. Therefore, your employer is obligated to withhold at a single rate and sometimes with zero exemptions. To avoid any kind of withholding, it is a good idea to give your employer Form W4 immediately, right at the start of your job. | ||||||||||||||||||||||||||||||||

| As we have already mentioned, even if you don't make enough money to file a tax return, you should still file if you qualify for the Earned Income Credit, even if you have no dependents. Even if you just earned $1, and if you are single, head of household, or qualifying widow or married with no dependents you can get 2 dollars back as an Earned Income Credit amount. If you have dependents and you only earned $1 for example, you can get anywhere from $9 to $11 back as an Earned Income Credit amount. If you look at the EIC tables you can see the different income scenarios. Look at the Earned Income Credit qualification rules to see if you qualify for the Earned Income Credit and for how much you qualify. | ||||||||||||||||||||||||||||||||

| You must file a tax return if you owe any self-employment tax. Usually you would owe self-employment tax if your net earnings from self-employment income are at least $400. So after you have calculated your total employment income and deduct the business expenses, you will be liable for self-employment tax if your net earnings from self-employment is $400 or more and you also must file a tax return. If your net earnings from self-employment are less than $400, you should file a tax return anyways to reconcile any 1099-Misc tax forms which you may have received from other businesses or individuals. Say you have received $50,000 in total from all the people you do business with and all your expenses and deductions for different items such as equipment, your net income is less than $400 or even at a loss, you should let the tax agencies know that you are operating below the $400 and avoid them asking you why you have not filed. It could be as simple as replying to their letter that you have net earnings of less than $400. | ||||||||||||||||||||||||||||||||

| Recordkeeping requirements | ||||||||||||||||||||||||||||||||

|

Whether

you prepare your return yourself or retain a professional tax preparer, you must

collect and organize your tax records. You cannot prepare your tax return unless

you get your personal tax data in order. Good records will help you figure your

income and deductions and will serve as a written record to present to the IRS

in the event that you are audited. Review your statements from banks,

employers, brokers, and governmental agencies on their respective Form 1099.

Check their work for miscalculations, additions, and omissions. It is also good

to keep your tax records so that you can review your tax returns and see what

has been done. Reviewing your tax returns from prior years will help you refresh

your memory as to how you handled income and expenses in prior years. This

review will also remind you of deductions, carryover losses, and other items you

might otherwise have overlooked that you might be eligible for. To maximize tax-savings opportunities, you must keep good records through the year. Good recordkeeping makes it easier to prepare your tax return, reduces errors, and provides a defense to any challenge from the Internal Revenue Service. There are many things you can do to keep good records or to make your recordkeeping easier to handle such as:

There are certain record keeping requirements you must meet in case the IRS needs to review your tax records later on. There are certain obligations to keep records and this depends on your tax situation. Claiming certain deductions and credits require you to keep records. Sometimes you can opt for standard deductions on certain items such as the standard deduction, standard mileage deduction, and even if you claim office in the home, there is a standard amount you claim and that way you don't have to worry about the record keeping requirements as much. You just select a standard amount of $5 per square footage in that case, just to provide you an example. There are so many brilliant ways to cut your taxes, to legally avoid paying taxes. Although the Tax Cuts and Jobs Act has come up with many tax incentives and many ways to disallow certain tax items, it has either allowed or neglected to disallow others. You can look really closely at almost every item in the new tax law and you will find ways to legally save money on your taxes. Whatever tax saving skill you manage to come up with requires that you show proof. To show proof or to prove your deductions, you must keep excellent business records. The IRS and new Tax Cuts and Jobs Act (TCJA) know exactly how difficult it is for some people to keep good records and that is why there are options for taking the standard - the standard deduction instead of itemizing, for example. Another one of these is using the cash method of accounting to avoid inventory recordkeeping obligations. If you are in the cash method of accounting business, you can be excused from the chore of doing inventory accounting for your business. If you are claiming the office in the home deduction, you can claim it by using the standard method which requires that you keep detailed records of all your expense or you can use the simplified method which gives you a flat rate to deduct that is much easier to calculate than the standard method. You are allowed to deduct $5 per square foot of your home office area. However, you are limited to only $1,500. Therefore, it is probably more beneficial to you to use the other methods which require that you keep more detailed records. Sometimes the methods that require more effort are more beneficial. How long to keep records? It depends.

If you own property, you may want to keep your tax records to show proof of depreciation deductions if you property is used for business. Also, when you sell your property, you must be able to show how you came up with the adjusted basis. Once you dispose of your property, then you must keep your tax records for at least 3 years, unless other conditions apply. There are other reasons you may want to keep your tax records for longer periods of time than required by the Internal Revenue Service. For example, you insurance company may need to ask you for these tax records a longer period than the Internal Revenue Service does. You probably should not be in too much of a hurry to get rid of your tax records. Nowadays it is easy to keep tons of paperwork stored in the cloud since you don't need any physical space to keep these records. Maybe the only ones that should want to get rid of tax records are tax professionals. In that case, you as a tax professional should keep tax records readily available to be copied for as long as your client is legally required to keep them. There are certain record keeping requirements you must meet in case the IRS needs to review your tax records to prove your deductions, but also you must keep a copy of your tax returns for a certain period of time as dictated by the Internal Revenue Service. The time to keep these tax return records varies depending on your filing situation but it normally is a minimum of 3 years or more time if you own property. If you own property, you are not necessarily obligated to keep the tax records forever, but you do need to be able to provide records for the basis of the property when you sell it. Maybe, if you never sell your property you don't have to worry about it, but no one really knows what is to come. There are many reasons why you may have to sell your property in the future. If you have made nondeductible contributions to a traditional IRA, keep a record of both your nondeductible and deductible contributions. This will help you when withdraw IRA money to figure the tax-free and taxed parts of the withdrawal. Also keep records of contributions and conversions to Roth IRA's and myRAs. You should also keep copies of Form 8606 and Form 5498 for these purposes. |

||||||||||||||||||||||||||||||||

| There are the costs of keeping up a home worksheet for example, where you list all expenses associated with the upkeep of your home. This worksheet will help you determine if you have paid more than the expenses of keeping up a home for a parent or your dependent children. It is usually useful when you are trying to determine if the individual is head of household for purposes of the head of household filing status. Items that are taken into consideration in this worksheet are property taxes, mortgage interest, rent, utilities, repairs, property insurance, food consumed in the home and other household expenses. Once you add up all the expenses and take into account what you have paid and what others have paid, then you determine if you paid more than 50 percent of the upkeep or not. If the total amount you paid is more than the amount others paid, you have met the requirement of paying more than half the cost of keeping up the home. Consequently, you must always make sure you create a paper trail for every credit or deduction you claim on your tax return. | ||||||||||||||||||||||||||||||||

| With the start of hurricane season, the Internal Revenue Service encourages individuals and businesses to safeguard their records against natural disasters by taking a few simple steps. The Internal Revenue Service advices to create a backup set of records electronically, store them in a safe place that is stored away from the original set. It is a good idea to store your backup records to the cloud where they will not burn or be destroyed by any natural disaster. Keeping a backup of records - including bank statements, tax returns, insurance policies, etc. - is easier now that many financial institutions provide statements and documents electronically. With documents in electronic form, taxpayers can save them to the cloud, download them to a backup device such as an external hard drive or USB flash drive. Furthermore, when keeping electronic records, taxpayers can burn a copy of them to a CD or DVD. | ||||||||||||||||||||||||||||||||

| As a tax preparer you must keep a record of the tax returns which you prepare. If there is a problem with the tax return later on, you must be able to produce a copy either to the Internal Revenue Service or to the client. The client may need a copy of the tax return because he or she lost the copy you provided when you prepared the tax return the first time. They may need to show the bank a copy for the last three years in order to qualify for a mortgage and they may need to look you up and ask you to provided them with another copy. Alternatively, they may request the copy from the Internal Revenue Service but this usually takes longer. You, as a tax preparer are legally required to provide a copy upon your tax client's request. You can charge for the copy but you must be able to produce it upon request. By the way, the charge for providing a copy must be nominal or reasonable. You should not be charging $900 for a copy of the tax return, for instance. | ||||||||||||||||||||||||||||||||

| Filing Status | ||||||||||||||||||||||||||||||||

|

If more than one filing status applies to you, choose the one that will give you the lowest tax. Your filing status is the filing status that applies to you at the last day of the year. If you obtained a divorce on December 26, 2018 and at the time of your divorce in 2018 you intended to and did remarry each other on August of 2019. You and your spouse must file your tax return as Married Filing Jointly or Married Filing Separately. Nice try! The Internal Revenue Service is already in the know about this trick. There is an easier way to do this. Choose the filing status which will give you the lowest tax but do it legally. You and your spouse must file your tax return as married filing jointly or married filing separately. The Internal Revenue Service is well aware of the "get married in December and divorce in January" trick. Unbelievable that this was a trick that some taxpayers pulled some time ago. Anyways, choose the best filing status that applies to you and do it honestly. No tricks! |

||||||||||||||||||||||||||||||||

| Your filing status generally depends on whether you are single or married at the end of the year. You could be married in March and could have become single by the end of the year. What matters is what is true on December 31st. Therefore, if you could benefit on your taxes by getting married on the last day of the year, then get married. However, stay married! The IRS has no problem with you getting married at the end of the year as long as you stay married. This could be considered legal tax planning and it is totally fine. As long as you are not going to divorce the following month and try the same scheme every December 31st, this is perfectly fine. | ||||||||||||||||||||||||||||||||

| You must determine your filing status before you can determine your filing requirements, the standard deduction and your correct tax. You can choose the Married Filing Jointly filing status if you are married and both you and your spouse agree to file together. When you use this filing status, you report your combined income and deduct your combined allowable expenses. You can file using the married filing jointly filing status even if you had no income or deductions. If you lived apart at the end of the year, it may be worthwhile to look into the head of household filing status instead. If the total amount you paid is more than the amount others paid, you meet the requirement of paying more than half the cost of keeping up the home to qualify for the head of household status. This of course is one of the many requirements to qualify for the head of household filing status. One of these is that you did not live with your spouse at any time during the last six months of the year. | ||||||||||||||||||||||||||||||||

| If your spouse died during the tax year, you are considered married for the whole tax year for filing status purposes. If you remarried before the end of the tax year, you must file a joint tax return with your new spouse and therefore the only option for your deceased spouse would be married filing separate. | ||||||||||||||||||||||||||||||||

|

Head of household |

||||||||||||||||||||||||||||||||

|

In qualifying for head of household filing status and in calculating the expenses of keeping up a home, include in the cost of upkeep expenses such as rent, mortgage interest, real-estate taxes, insurance on the home, repairs and utilities, and food eaten in the home. The cost of upkeep expenses for calculating the cost of upkeep expenses would not include the rental value of a home you own. |

||||||||||||||||||||||||||||||||

|

To qualify for Head of Household filing status, you must be

unmarried or considered unmarried at the end of the year. They say that the

Head of Household filing status is one of the most misunderstood tax filing

statuses. It seems to be one of the most misunderstood because so many

individuals abuse this filing status for the benefits it allows. For

example, many married individuals abuse this filing status by saying that

they qualify to be considered unmarried for tax filing purposes so they can

receive credits that they would otherwise not qualify for if they use the

married filing separate filing status.

The due diligence requirement that has always been in place for the Earned Income Credit is also now in effect for the head of household filing status. There is a now a record keeping requirement under IRC section 6695(g) that includes a paper trail requirement for determining a client's eligibility to file as head of household. If you don't show how you qualified your client for the head of household filing status by asking the correct questions, the IRS imposes a $500 penalty for each failure. These are the same due diligence requirements already in place on Form 8867 for the child tax credit, the American opportunity tax credit and the earned income credit. Many misuse the Head of Household filing status in order to get a higher Earned Income Credit amount, for example. Therefore, to qualify for head of household you must be unmarried or be considered unmarried. You must have paid more than half the cost of keeping up a home for the year and have a qualifying person who lived with you for more than half of the year unless this person is your parent. Add up the amounts contributed and if you amount is more than half the amount others paid, you meet the requirement of paying more than half the cost of keeping up the home to qualify for the head of household status. If you think you qualify for the head of household filing status, fill out the worksheets and follow the rules. It is worth your try because doing so will give you a lower tax rate than those for single or married filing separately. This would also allow you better credits and higher deductions too. |

||||||||||||||||||||||||||||||||

| Follow the tax rules to the dot. According to the IRS, the Head of Household filing status is for single or unmarried taxpayers who keep up a home for a qualifying person. The Head of Household filing status has some important tax advantages over the single filing status such as a lower tax rate and a higher standard deduction amount than for a single taxpayer. To qualify for Head of Household, you must meet certain filing requirements. First, you must not be married and if you are married, be considered unmarried for tax filing purposes. Second, you must have paid more than half the cost of keeping up a home for the year for a qualifying person. The qualifying person must have lived with you in the home for more than half the year. You don't want to be caught breaking the tax rules to gain a tax advantage for your clients. Follow the tax rules to the dot and avoid trouble with the Internal Revenue Service. | ||||||||||||||||||||||||||||||||

| You may be eligible to file as Head of Household if the individual who qualifies you for this filing status is born or dies during the year. The period for which the child was not present in the home can be considered as if he or she was there as long as it pertains to these reasons. You are considered to have provided more than half of the cost of keeping up a home for this individual if your qualifying child or qualifying relative lived with you for more than half the year he or she was alive. If the dependent is your parent, for whom you paid for the entire part of the year he or she was alive, more than half the cost of keeping up a home in which he or she lived in, then this parent can still qualify your for the head of household filing status. | ||||||||||||||||||||||||||||||||

|

If you live apart from your spouse and meet certain tests, you may be able to file as head of household, even if you are not divorced or legally separated. One of the requirements to file as Head of Household, you must not have lived with your spouse at any time during the last six months of the year. Very important to know is that if you are married and if you qualify, you can practically use any filing status except single. If you are married, you would not use the qualifying widow (or widower) filing status, of course. |

||||||||||||||||||||||||||||||||

| If your taxable income is more than $100,000 you cannot use form 1040EZ or Form 1040A. You are generally stuck and must use Form 1040. | ||||||||||||||||||||||||||||||||

| One of the requirements for the head of household filing status is that you pay for the upkeep of a home for your qualifying dependent. In qualifying for head of household filing status and in calculating the expenses of keeping up a home, include in the cost of upkeep expenses such as rent, mortgage interest, real-estate taxes but do not include the rental value of a home you own. You can include insurance on the home, repairs and utilities and also food eaten in the home. You may be eligible to file as head of household if the individual who is born or dies during the year qualifies you for this filing status and you must have provided more than half of the cost of keeping up a home which was the individual's main home for the period when the individual lived. | ||||||||||||||||||||||||||||||||

| Not all dependents have to live you in order for you to qualify for the head of household filing status. You can qualify for the head of household filing status if you have a qualifying child or if you support your parent's home. For Head of Household filing purposes, if your father is your qualifying relative and he does not live with you, you must pay more than half the cost of keeping up his home for the entire year. For dependents who don't need to live with you to qualify you as head of household, you must support a home for them for more than half the support of the home in which you both live in order to claim the head of household filing status. This is just one of the requirements - there are many others. | ||||||||||||||||||||||||||||||||

| There are other requirements to determine head of household qualifications. For example, you must determine who is a qualifying person that would qualify you to file as head of household. If the person is your qualifying child and he or she is single, then that person is a qualifying person. A qualifying child can be a son, daughter, grandchild who lived with you more than half the year and also has to meet other tests. If this qualifying child is married and you can claim an exemption for him or her, then this person would also be a qualifying person. However, if you cannot claim an exemption for him or her, then normally you cannot consider him or her a qualifying person for the head of household filing status. | ||||||||||||||||||||||||||||||||

| If you are able to claim your mother or father, maybe you can qualify for the head of household filing status. If the person is your qualifying relative who is your father or mother and you can claim an exemption for him or her, they are a qualifying person that can qualify you for the head of household filing status. Additionally, your parents can live in their own home - a home which you have supported for more than half of the upkeep. However, you must be able to claim an exemption for your parent and if you cannot claim an exemption for him or her, then they are not to be considered a qualifying person. You must be able to claim an exemption for your dependent in order to claim him or her for the head of household filing status. | ||||||||||||||||||||||||||||||||

|

If your child is considered temporarily absent from home, you can still claim him as living with you if he is away because of illness, vacation, education, military service or if the child is away on a business trip. |

||||||||||||||||||||||||||||||||

| You may be eligible to file as Head of Household even if the child who is your qualifying person has been kidnapped. You can claim Head of Household filing status if the child is presumed by law enforcement authorities to have been kidnapped by someone who is not a member of your family or the child's family. Also in the year of kidnapping, the child must have lived with you for more than half of the year before the kidnapping. Additionally, you must have met the requirements or would have met the Head of Household filing status requirements if the child had not been kidnapped. The same goes for children that are born or who die during the year. You may be eligible to file as Head of Household if the individual who qualifies you for this filing status is born or dies during the year. You are considered to have provided more than half of the cost of keeping up a home for this individual if you provided more than half the support for the part of the year he or she was alive or half the cost of keeping up the home he she lived in. | ||||||||||||||||||||||||||||||||

| Furthermore, for Head of Household filing purposes, if your father is your qualifying relative and he does not live with you, you must pay more than half the cost of keeping up his home for the entire year. Also, in some circumstances, you do not have to claim a child as dependent to qualify for the Head of Household filing status. For example, a custodial parent may be able to claim Head of Household filing status even if he or she released a claim for exemptions for the child. | ||||||||||||||||||||||||||||||||

|

If your qualifying relative is not related to you in one of the ways for relatives who do not have to live with you, and they are a qualifying relative only because he or she lived with you all year as a member of your household, then they are not a qualifying person for you to use the head of household filing status. Almost in all cases, if you cannot take an exemption for a qualifying relative, they cannot be a qualifying person for you to benefit from the head of household filing status. It is in your best interest for you to opt for the head of household filing status. This filing status can give you a greater tax benefit than the single or married filing separately filing statuses. |

||||||||||||||||||||||||||||||||

| Get familiar with the terms qualifying child and qualifying relative as they have different tests and requirements that you must meet for the different credits or deductions to take on your tax return. A person, qualifying child or qualifying relative cannot qualify more than one taxpayer for the head of household filing status in a single year. A child does not qualify you for the head of household filing status if he or she is your qualifying child for exemption purposes only as is sometime the case with divorced, legally separated parents or custodial parents. In certain circumstances, the child can be your qualifying child to claim the head of household purposes and not be your child for whom you can claim an exemption. Additionally, if you can claim an exemption for a person only because of a multiple support agreement, that individual is not a qualifying person who can qualify you for the head of household filing status. | ||||||||||||||||||||||||||||||||

| The correct form | ||||||||||||||||||||||||||||||||

|

You should be concerned with filing the appropriate form for the tax situation. Even if everything does fit into Form 1040, you should file the correct forms with the Internal Revenue Service. You can use Form 1040EZ if your filing status is Single or Married Filing Jointly, your taxable income is less than $100,000, and you are not a debtor in a Chapter 11 bankruptcy case filed after October 16, 2005. There is a fantastic analogy in a Tax Act blog "The Difference Between Form 1040, 1040A and 1040EZ" for using the various tax forms. Filing the three different kinds of returns 1040EZ, 1040A, and 1040 is like having three water glasses of different sizes where Form 1040EZ would be an 8 ounce glass, 1040A would be a 12 ounce glass and Form 1040 would be a 24 ounce glass. Just like you can use a 24 ounce glass to drink 8 ounces, 12 ounces or 24 ounces of water, you can use Form 1040 to file tax returns that can be filed on Form 1040EZ and Form 1040A. However, just like you cannot drink 24 ounces of water from an 8 ounce or 12 ounce glass (in one filling), you cannot file a Form 1040 or 1040A tax return on a Form 1040EZ or a Form 1040 tax return on a Form 1040A. You get the idea? |

||||||||||||||||||||||||||||||||

| Form 1040EZ | ||||||||||||||||||||||||||||||||

|

Form 1040EZ is the easiest tax form there is. Form 1040EZ is usually the first tax form that a taxpayer files after they get their first job. There are many items that allow your to use Form 1040EZ. You can only file as single or married filing jointly when you use Form 1040EZ. You are not allowed to claim any dependents on Form 1040EZ. You must also be under age 65 and not blind on January 1, 2019. The items of income you can report on Form 1040EZ can only be from wages, salaries, tips, taxable scholarships and fellowship grants. You can only report your unemployment compensation or Alaska Permanent Fund dividends on Form 1040EZ. Just how Form 1040EZ is a very simple form to fill out, it is also very limited as to what you can include. |

||||||||||||||||||||||||||||||||

| If your interest earnings are not that much, you can use Form 1040EZ. If your taxable interest income was not over $1,500, you can file your tax return on Form 1040EZ. If your interest income is over this amount, sorry, but you must file Form 1040A or Form 1040. In order to file Form 1040EZ, your total taxable income has to be less than $100,000. If you have tips, your tips must be only tips which are included in boxes 5 and 7 of your Form W-2. Additionally, you cannot have household employment taxes to use Form 1040EZ. Other items to consider when considering if you can file Form 1040EZ is that you cannot have had a Chapter 11 bankruptcy case that was filed after October 16, 2005 to report on your tax return. You also cannot have any adjustments to income. Your credits are limited only the Earned Income Credit. Furthermore, you cannot include any advanced payments of the premium tax credit on Form 1040EZ. | ||||||||||||||||||||||||||||||||

| If your spouse is a nonresident alien, you cannot use Form 1040EZ if he or she cannot file a U.S. tax return. If your nonresident alien spouse has a social security number or an Individual Tax Identification Number, that would normally mean that they are a resident, otherwise they would normally not have qualified for such an identification number. If your nonresident alien spouse becomes a resident alien before he or she can file a tax return, then you would be able to meet the requirements and be able to file Form 1040EZ. Likewise, if your nonresident spouse is living with you in the United States and files with you jointly, he or she would be able to qualify for an Individual Identification Number with the Internal Revenue Service and therefore be considered a resident alien instead of a nonresident alien. | ||||||||||||||||||||||||||||||||

|

You also cannot file a tax return using Form 1040EZ if you owe tax from the recapture of an education credit. If you can claim a credit for excess social security and tier 1 RR TAX withheld you will not be able to file Form 1040EZ either. There will also not be any space for any retirement Savings Contributions Credit or the Saver's Credit on Form 1040EZ. Therefore, if you have any of these, you will not be able to file Form 1040EZ. Credits are limited only the Earned Income Credit with no children. |

||||||||||||||||||||||||||||||||

| There are only certain items you can fit on Form 1040EZ. Just like you cannot fill 12 ounces of water into an 8 ounce glass, you cannot fill your Form 1040EZ with certain items meant for Form 1040. You can try it and in both instances would result in a mess. In the glass of water instance, you would have to mop the floor and the Form 1040EZ instance, you would not find a space for it and if you insert it in the form anyways, you would soon receive a letter from the Internal Revenue Service (IRS) to let you know of the error. Just like you want to keep that floor dry, you want to keep the Internal Revenue Service (IRS) or the other tax collecting agencies away. It is not a bad thing in itself that the IRS contacts you. Only that they are quite busy and if they really have to contact you is because of trouble with your tax return. | ||||||||||||||||||||||||||||||||

| Form 1040A | ||||||||||||||||||||||||||||||||

|

You can use Form 1040A if you only had income from wages, salaries, or tips. You can use 1040A if your only adjustments to income you want to claim is a student loan interest deduction. You can also file 1040A if you received dependent care benefits or if you owe tax from the recapture of an education credit or the Alternative Minimum tax. However, you cannot use Form 1040A if you received income from self-employment such as from your business or your farm. If you have self-employment income, you must use Form 1040 and the other corresponding tax forms. |

||||||||||||||||||||||||||||||||

| Taxpayer Identification Numbers | ||||||||||||||||||||||||||||||||

|

An Individual Tax Identification Number (ITIN) does not entitle you to social security benefits and neither does it allow you to work legally under U.S. law. An ITIN is only intended to serve the purpose of identifying the individual filing a tax return or being claimed on a tax return for various purposes such as when claiming an exemption. It is in the same format as a social security number. Although an individual taxpayer identification number (ITIN) is like a social security number in format, unlike a social security number which serves many purposes, the ITIN number only serves one - identifying the holder. The individual tax identification number (ITIN) does not entitle the holder for social security benefits or to legally work in the United States. If you are working in the United States illegally and someday will have a status adjustment, you should keep all your paystubs to report all your wages to the Social Security Administration to the correct social security number when your legal status becomes adjusted. This is such an oxymoron! In one part of the tax law we are stating that using someone else's taxpayer identification is tax identity fraud and in another part we are letting them file tax returns with form W-2s that have fraudulent social security numbers on them. |

||||||||||||||||||||||||||||||||

|

Everyone needs a number. TIN numbers are unique. Names are not unique to an individual and that is why we use numbers instead. Search for a name on Facebook, including both the first name and last name and you will probably get at least ten people with the same name. If you are a nonresident or resident alien and you do not have and are not eligible to get an SSN, you must apply for an ITIN. You must have an Individual Tax Identification Number (ITIN) in order to file their tax return. It must be noted and it is extremely important that this identification is only used for tax filing purposes. A Taxpayer Identification Number (ITIN) is an identification number issued by the Internal Revenue Service that is only made available for certain nonresident and resident aliens, their spouses, or dependents who are not eligible to get a Social Security Number (SSN). It is in the same format of the social security number with nine digits. Many undocumented taxpayers make the mistake of giving this number to their employers but they should never do this. The employer is under the obligation to end their employment on the spot if the employee shows them this Internal Revenue Service issued identification card. This is like making a confession to their employer that they are indeed working illegally in the country. In turn if the employer continues their employment, such employer would run into trouble with the immigration service. This could mean huge penalties for the employer for not complying with the immigration laws. |

||||||||||||||||||||||||||||||||

| If your spouse is a nonresident alien, he or she must have either an SSN or an ITIN if you file a joint tax return. He or she must also have either an SSN or an ITIN if you file a separate tax return and claim an exemption for your spouse or if your spouse is filing a separate tax return. The Taxpayer Identification Number (ITIN) is an identification number used by the Internal Revenue Service (IRS) in the administration of tax laws. The Internal Revenue Service issues other numbers too, such as the Social Security Number "SSN", the Employer Identification Number in addition to the Individual Taxpayer identification Number "ITIN". These numbers are what identify you and your dependents and your business on your tax return. | ||||||||||||||||||||||||||||||||

|

An ITIN must be furnished on returns, statements, and other tax related documents. This number must be furnished when filing your returns or when claiming tax treaty benefits. Also an ITIN must be on a withholding certificate if the beneficial owner is claiming tax treaty benefits other than from income from marketable securities. This number must also be on a withholding certificate if the beneficial owner is claiming exemption for effectively connected income or exemption for certain annuities. |

||||||||||||||||||||||||||||||||

| Furthermore, you generally must list the social security number (SSN) of any person for whom you claim an exemption on your individual income tax return. If your dependent or spouse is not eligible to get a SSN, you must list an ITIN instead. | ||||||||||||||||||||||||||||||||

|

However, let's say you qualify for an SSN instead. You should apply for a SSN by completing Form SS-5, Application for a Social Security Card, and also submit evidence of identity, age and citizenship or lawful alien status. The IRS requires a Taxpayer Identification Number (TIN) as an identification number for the administration of the tax laws. You can acquire this number from the Social Security Administration (SSA) or by the Internal Revenue Service (IRS). Only the Social Security Administration can issue a Social Security number and all other taxpayer Identification numbers are issued by the Internal Revenue Service (IRS). It seems that we mentioned all the possible TINs and here they are again just in case we missed them. The taxpayer identification numbers available are social security number (SSN), the Employer identification number (EIN), Individual taxpayer identification number (ITIN), the taxpayer Identification number for pending U.S. Adoptions (ATIN), and the preparer tax identification number (PTIN). The previously assigned temporary IRS Preparer Tax Identification Numbers are no longer valid. |

||||||||||||||||||||||||||||||||

| If questions 11 through 17 on Form SS-4 do not apply to the applicant because he has no U.S. tax return filing requirement, such questions should be annotated "N/A". A foreign entity that completes Form SS-4 in the manner described above should be entered into IRS records as not having a filing requirement for any U.S. tax returns. However, if the foreign entity receives a letter from the IRS soliciting the filing of a U.S. tax return, the foreign entity should respond to the letter immediately by stating that it has no requirement to file any U.S. tax returns. Failure to respond to the IRS letter may result in a procedural assessment of tax by the IRS against the foreign entity. If the foreign entity later becomes liable to file a U.S. tax return, the foreign entity should not apply for a new EIN, but should instead use the EIN it was first issued on all U.S. tax returns filed thereafter. | ||||||||||||||||||||||||||||||||

|

The ITIN number is not a SSN! It is only used to file your tax returns with it. You should probably also not use your ITIN to open credit with it. Maybe it would work and since SSNs are not yet in the 900 series, doing so does not seem to pose a legal problem. However, the purpose of an ITIN is to file your tax returns. |

||||||||||||||||||||||||||||||||

| The ITIN is a tax processing number only available for certain nonresident and resident aliens, their spouses, and dependents who cannot get a Social Security Number (SSN) that begins with the number 9 in the SSN format. To deter any use of the ITIN for an impermissible purpose, the IRS carefully screens to whom they issue this number. | ||||||||||||||||||||||||||||||||

|

To obtain the ITIN, you must complete Form W-7. In addition,

you must substantiate your foreign or alien status and true identity by

mail. Alternatively, you can substantiate foreign or alien status and true

identity by going through an Acceptance Agent authorized by the IRS. If you

need to apply for a number, you can visit Acceptance Agents which are

entities (colleges, financial institutions, accounting firms, etc.) who are

authorized by the IRS to assist applicants in obtaining ITINs. An ITIN, or

Individual Taxpayer Identification Number is a 9-digit number, beginning

with the number 9 and formatted like an SSN. It is important that you be

aware that you cannot claim the earned income credit using an ITIN.

Except that for now there is a new credit under the new TCJA tax law. There is a new $500 nonrefundable credit for dependents other than a qualifying child or for a qualifying child without the required SSN. If you qualifying dependent only has an ITIN, then you can still claim $500 of the Earned Income tax credit and this is a nonrefundable credit. |

||||||||||||||||||||||||||||||||

| You must furnish a Taxpayer Identification Number (TIN) on your income tax returns and all required documents when filing your tax return. You will also be asked for a Taxpayer Identification Number (TIN) when you contact the Internal Revenue Service (IRS) either on the phone or on any correspondence by mail. Also, a Taxpayer Identification Number (TIN) must be provided when you file your tax returns or when claiming treaty benefits. Furthermore, a Taxpayer Identification Number (TIN) must be on any withholding certificate for claiming tax treaty benefits, exemption of effectively connected income, or exemption for certain annuities. | ||||||||||||||||||||||||||||||||

|

In addition, a Taxpayer Identification Number (TIN) must also be provided when claiming exemptions for your dependents or your spouse. You generally must list on your tax returns the Social Security number (SSN) or Individual Taxpayer Identification number (ITIN) for any person for whom you are claiming an exemption. You can use either the Social Security Number that was issued by the Social Security Administration or the Individual Taxpayer Identification number (ITIN) that was issued by the Internal Revenue Service (IRS). If the child was born or if the child died in the same year, you don't need a social security number. If the child was born in that year, you should probably apply for a number since it only takes about two to four weeks to receive the Social Security Number from the Social Security Administration or the Taxpayer Identification Number (TIN) from the Internal Revenue Service (IRS). These time frames vary depending on the SSA or IRS specifications or service areas. If the child died in the same year he or she was born, then instead of a Social Security Number or an Individual Identification Number (ITIN), attach a copy of the child's birth certificate and write "Died" in the appropriate exemption line of the tax return. |

||||||||||||||||||||||||||||||||

|

So just to recap, you can acquire a Taxpayer Identification Number in various different ways. If you need a Social Security Number from the Social Security Administration, you will need to complete Form SS-5, Application for a Social Security Card. In addition to filling out Form SS-5, you must also submit evidence of your identity, age, and of your U.S. citizenship or lawful alien status. You can get Form SS-5 by calling the Social Security Administration office or on the Web. If you have a business you can acquire an Employer Identification Number (EIN) from the Internal Revenue Service (IRS). This number is also known as a federal identification number. This number is normally used to identify your business entity. You can acquire this Employer Identification number even for your sole proprietor business but normally it is only given to a sole proprietorship if the sole proprietor has employees. Sole proprietors can use their Social Security number to report their business activities to the Internal Revenue Service (IRS) and are not obligated to get an Employer Identification number (EIN). The Employer Identification Number is also used by estates and trusts whom are required to report their income on Form 1041, U.S. Income Tax Return for Estates and Trusts. |

||||||||||||||||||||||||||||||||

| If you, your spouse or your dependents are not legally able to acquire a Social Security Number (SSN), you can apply for an ITIN, Individual Taxpayer Identification Number. This Individual Taxpayer Identification Number is only available for certain nonresident and resident aliens, their spouses and dependents who cannot get a Social Security Number (SSN). This number starts with a 9 in the same format at the Social Security Number (SSN). The Individual Taxpayer Identification Number is only for reporting purposes and does not authorize the individual for any benefits such as the Earned Income Credit. Nor does this ITIN authorize the individual to work in the United States. | ||||||||||||||||||||||||||||||||

| You can get an Individual Taxpayer Identification Number (ITIN) by completing IRS Form W-7, IRS Application for Individual Taxpayer Identification Number. Additionally, you are required to furnish documentation substantiating your foreign or alien status and your true identity or the true identity of your spouse or your dependents. You can walk in your documents to an IRS office, mail it to the IRS, or you can process your application through an Acceptance Agent authorized by the Internal Revenue Service. Acceptance Agents such as colleges, financial institutions and accounting firms who are authorized by the Internal Revenue Service (IRS) assist applications in obtaining their Individual Identification Numbers (ITINs). Once they gather the application and all the required paperwork, they will forward everything to the Internal Revenue Service for processing. | ||||||||||||||||||||||||||||||||

| Foreigners who are individuals should either apply for a Social Security Number (SSN) if they meet the requirements for one Form SS-5 with the Social Security Administration or they should apply for an Individual Taxpayer Identification Number (ITIN) on Form W-7. Each applicant for an ITIN no longer needs to attach a copy of tax return when submitting your Form W-7. However, you will need to attach the other required identification documentation. | ||||||||||||||||||||||||||||||||

| If you have applied to adopt a child or are in the process of legally adopting a U.S. citizen or resident child but who cannot get a Social Security for that child in time to file your tax return, you can apply for an Adoption Taxpayer Identification Number (ATIN) for that child. This is a temporary nine-digit number issued by the Internal Revenue Service to temporary provide a number when you are in the process of adopting your child. Use Form W-7A, Application for Taxpayer Identification Number for Pending U.S. Adoptions to apply for an ATIN. However, you cannot use Form W-7A or go through this application process if the child is not a U.S. citizen or resident. Apply for an ITIN instead for the child. | ||||||||||||||||||||||||||||||||

|

Foreign entities that are not individuals (i.e., foreign corporations, etc.) and that are required to have a federal Employer Identification Number (EIN) in order to claim an exemption from withholding because of a tax treaty (claimed on Form W-8BEN), need to submit Form SS-4 Application for Employer Identification Number to the Internal Revenue Service in order to apply for such an EIN. Those foreign entities filing Form SS-4 for the purpose of obtaining an EIN in order to claim a tax treaty exemption and which otherwise have no requirements to file a U.S. income tax return, employment tax return, or excise tax return, should comply with the special instructions when filling out Form SS-4. When completing line 7b of Form SS-4, the applicant should write "N/A" in the block asking for an SSN or ITIN, unless the applicant already has an SSN or ITIN. When answering question 10 on Form SS-4, the applicant should check the "other" block and write or type in immediately follow it with "For W-8BEN Purposes Only", or "For Tax Treaty Purposes Only", "Required under Reg. 1.1441-1(e)(4)(viii)" or "897(i) Election". |

||||||||||||||||||||||||||||||||

| Foreign persons who are individuals should apply for a social security number (SSN, if permitted) on Form SS-5 with the Social Security Administration or get an ITIN. Each ITIN applicant must now apply using the revised Form W-7. However, attaching a federal income tax return to the Form W-7 is no longer required. | ||||||||||||||||||||||||||||||||

| There is an identifying for almost any situation. For example, you must apply for an ATIN which is a temporary nine-digit number issued by the IRS to individuals who are in the process of legally adopting a U.S. citizen or resident child but who cannot get an SSN for that child in to file their tax return. | ||||||||||||||||||||||||||||||||

|