|

|

|

EA Tax Lesson 3 - Exemptions and Dependents

This tax lesson will teach you about exemptions which are personal exemptions and exemptions for dependents. You will learn how to calculate your exemptions when they are limited.Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

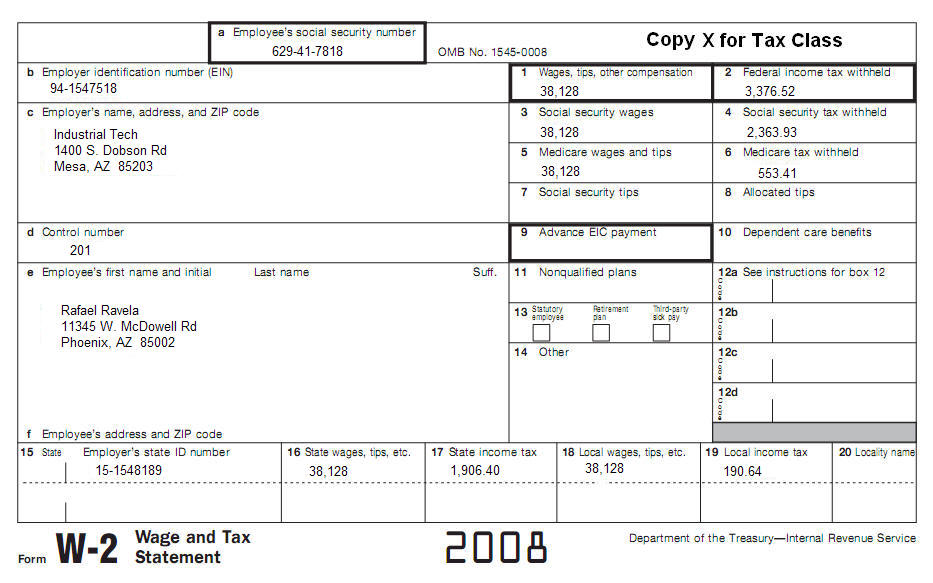

Use IRS Publication 17 Chapter 3, IRS Publication 501 and 1040A instructions to answer the following questions. Rafael supported his 18-year-old daughter, Abigail Garcia (SSN 602-94-1434) and she lived with Rafael all year while her husband Thomas Garcia (SSN 634-93-2342) was in the Armed Forces. Thomas' gross wages were over $40,000. Abigail and her husband file a joint return and they usually end up owing because they have no dependents. Rafael provided $4,000 toward the support of Maria Martinez (SSN 601-15-8724), his mother during the year. She had earned income of $600, nontaxable social security benefits of $4,800, and tax-exempt interest of $200. Maria used all these for her support. Rafael provided total support for his brother, Cesar Ravela (SSN 558-48-7812), who lived in Nejapa, El Salvador, for all of 2008. Cesar lived in the United States a number of years ago so he already has a social security number and Rafael would not have to apply for an ITIN number. Rafael provided total support for his wife Imelda Mejia (ITIN 901-15-7614) and his 2 children, Raul Ravela, age 4 (ITIN 901-15-7615) and Rosalinda Ravela, age 3 (ITIN 901-15-7617). His wife and children lived in Tijuana, Mexico for all of 2008.

Prepare a Federal Form 1040A return for Rafael Ravela. Get all his basic information from the following W2, including income information.

|

| Back to Tax School Homepage |