|

|

||||||||||||||||

|

Tax Lesson 16 - Child and Dependent Care Expenses Credit

|

||||||||||||||||

In this tax training topic you will learn how to claim a credit for child and dependent care expenses. You will become aware of the tests you must meet to claim the credit and how to figure and claim the credit. You may be able to claim the credit if you pay someone to care for your dependent who is under age 13 or for your spouse or dependent who is not able to care for himself or herself.Tax School Homepage Student Instructions: Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

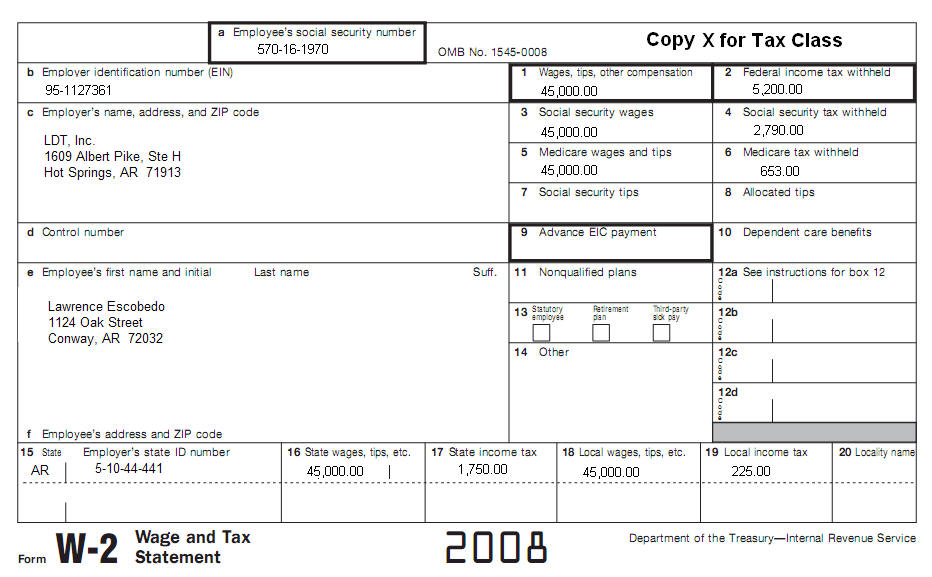

Use IRS Publication 503 to complete this topic. Complete a tax return for Lawrence Escobedo (570-16-1970) and Theresa Escobedo (502-39-4055). They got married December 31, 2008. Their Children who lived with them all year are:

Only Lawrence worked. Theresa did not work. Theresa attended school full time for 7 months in 2008. The school was not an on-the-job training course, correspondence school, night, or internet school. When she was in school they were taken care of by Happy Child, inc.:

Also figure the Child tax credit and enter on Form 1040A line 32. In addition to their earnings, they had the following:

Complete the Form 1040A, Schedule 2, Form 8812 and Schedule EIC. Use the following attached W2. All information on W2 is current.

|

||||||||||||||||

| Back to Tax School Homepage |