|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Back to Tax School Homepage | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Topic 19 - Self-Employment Income and Tax

In this tax topic you will learn the federal tax laws that apply to small business sole proprietors and to statutory employees. Here, you will be introduced to business income, business expenses and certain business tax credits to use in filing your business return. How do you know when you are self-employed? You are self-employed if you carry on a trade or business as a sole proprietor or as an independent contractor. In addition, in this topic you will be introduced to self-employment (SE) tax and you will learn how to figure the SE tax.Student Instructions:Print this page, work on the questions and then submit test by mailing the answer sheet or by completing quiz online. Instructions to submit quiz online successfully: Step-by-Step check list Answer Sheet Quiz Online

Most forms are in Adobe Acrobat PDF format.

Material needed to complete the sections in this assignment:

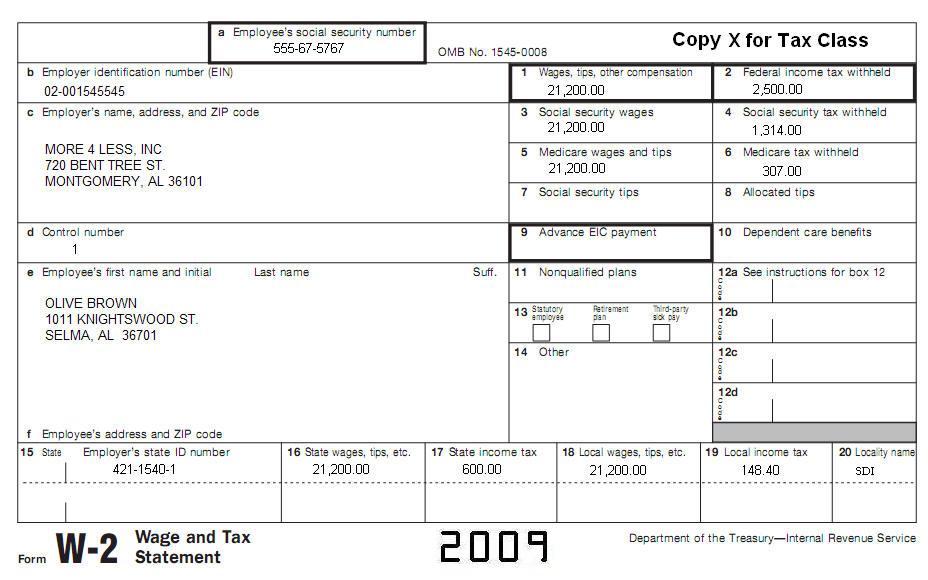

Please complete a return for Olive Brown. Prepare Form 1040, Schedule C , Schedule SE, Form 4562. Olive is a 27 year old unmarried taxpayer. She owns and manages Fashions At Discount (Activity codes). This is a clothing store she started in 2009. Address for business is 2304 Cobbs Ford Rd, Selma, AL 36701. She had the following for her store: Income Statement Year Ended December 31, 2009

Cost of Goods Sold

Expenses:

** Enter on line 17 of Form 4562 Inventory is valued at cost and there was no change in determining inventory at any time during the year. In addition, Olive had the following:

*Plan established under the business and she does not have any insurance at her work Olive paid rent all year in 2009. Use W2 for basic information. Address and other information on W2 is current.

Answer the following questions as accurately as possible.

A. $25,000.

6. Which of the following earnings is not subject to self-employment tax?

A. Gains and losses, by a dealer in options or commodities, from

dealing or trading in foreign currency contracts. 7. Hahn Company, a calendar year taxpayer operating as a sole proprietorship, reports Federal income taxes employing the accrual method of accounting. Hahn Company shows the following items of income and expense for 2009:

For 2009 year tax purposes, what is the amount of Hahn Company's net income reportable on Schedule C, "Profit or Loss from Business (Sole Proprietorship)"?

A. $122,500. 8. John has three employees who are certified as members of a targeted group. Two of the employees worked for John for 2 months in 2007 and came back to work for John on January 1, 2009. The other employee began working for John on January 1, 2009. Each employee makes $1,000 per month. How much can John claim as qualified first year wages in computing the Work Opportunity Credit?

A. $12,000. 9. Rob and George own an office building that was built in 1980. They opened a tax return business in 2008 and made numerous renovations during 2009 to the building to bring it into compliance with the Americans with Disabilities Act of 1990. They had gross receipts of $750,000 dollars and ten full-time employees during 2009 and they spent $15,000 in eligible access expenditures. What is the current year Disabled Access Credit?

A. $5,000. 10. Ryan runs a manufacturing business employing several people with young children. These employees require daycare as both parents work. He decided that, in order to make it easier for his employees to come to work each day, he would allocate some of the unused space in his manufacturing facility to a child care facility. In 2009, he incurred $20,000 in qualified childcare facility expenditures. He had no qualified childcare resource and referral expenditures and had no pass through credits. What is Ryan's credit for 2009.

A. $20,000. 11. The Investment Credit is:

A. A credit for purchasing a business. 12. In 2009, Santergraph, Inc. remodeled and converted a portion of their building into a licensed child care facility open for the care of any of their employee's children. The cost of this remodeling qualifies for which of the following:

A. An asset to be depreciated over the remaining useful life of the

building. 13. Maude has a small business that has a profit of $15,000. Her husband, Harold, has a farm that has a loss of $7,000. They are married. Which of the following is correct regarding their self-employment tax computation?

A. If they file separately, Harold may not elect to use the optional

method. 14. In 2009, Animor, a self-employed business man, has prepared payroll tax returns and income tax returns for Yethir, Inc. on a continuous basis. In 2009, Yethir, Inc. paid Animor $900 for his services. What is Yethir, Inc.'s reporting responsibility?

A. File a W-2 for $900. 15. Luck and Charm Partnership provides consulting services to the public. In 2009, the firm performed services and in exchange received a truck with a fair market value of $10,000, adjusted basis of $7,500: and also received lawn care services with a fair market value of $5,000. Luck and Charm uses the cash basis method for accounting purposes. What must Luck and Charm report as income for 2009?

A. $12,500. 16. The taxpayer earned $1,000 in interest in 2007. Taxpayer withdrew $700 in 2008 and $300 in 2009. How much of the original $1,000 should taxpayer report as interest in 2009?

A. $0. 17. Dawn meets the requirements for deducting expenses for the business use of her home. She uses 20% of her home for her business. She had the following income and expenses. What amount of depreciation will be allowed under the office in home deduction limitation rules?

A. $0. 18. Mary, a seamstress, made loans of $5,000 and $1,000 to Buttons & Bows and Thread Bare, respectively. Both of these establishments are partnerships. Mary also made a loan of $2,000 to her cousin Sarah, who was starting her own business as a proprietorship. The loans to both partnerships improved Mary's business, which was the reason Mary made the loans. If all three loans become uncollectible, what amount may Mary deduct as a business bad debt?

A. $5,000. 19. The F&E Partnership spent $100,000 on eligible access expenditures that qualify for the disabled access credit. The partnership had gross receipts of $1 million and 30 full-time employees during the preceding tax year. What is the amount of the disabled access credit for the year 2009?

A. $5,000. 20. You generally must file an income tax return for the year 2009 if your net earnings from self-employment is ____ or more.

A. $600.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Back to Tax School Homepage |